Over 2 million + professionals use CFI to learn accounting, financial analysis, modeling and more. Unlock the essentials of corporate finance with our free resources and get an exclusive sneak peek at the first module of each course. Start Free

Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. The two most common types of leases in accounting are operating and finance (or capital) leases. It is worth noting, however, that under IFRS , all leases are regarded as finance-type leases. This step-by-step guide covers the basics of lease accounting according to IFRS and US GAAP .

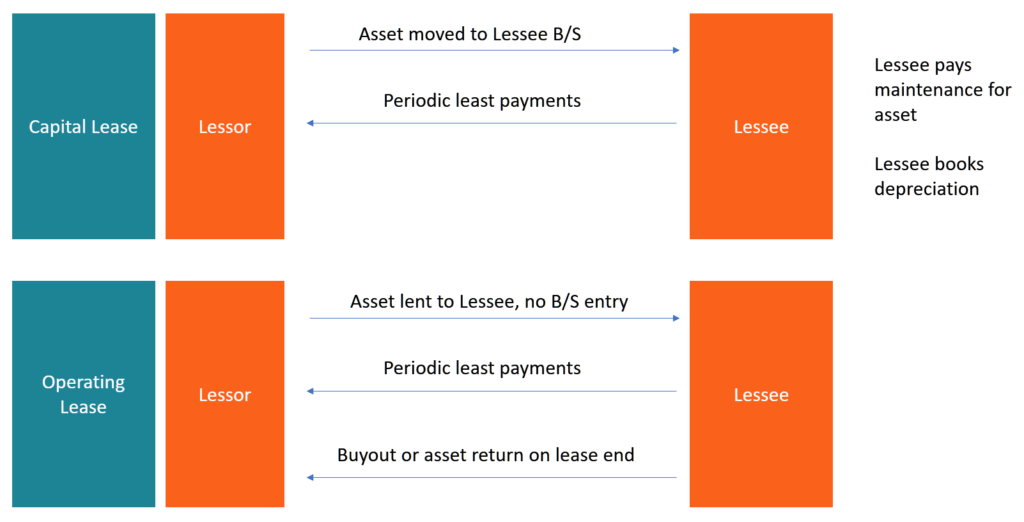

The two most common types of leases are operating leases and financing leases (also called capital leases). In order to differentiate between the two, one must consider how fully the risks and rewards associated with ownership of the asset have been transferred to the lessee from the lessor.

Recall that under IFRS, lease classification has been abandoned as a practice. Under ASPE and GAAP, a finance lease is called a capital lease. Otherwise, it is an operating lease, which is similar to a landlord and renter contract.

Whether the risks and rewards have been fully transferred can be unclear, so IFRS outlines several criteria to identify finance leases . At least one of the following conditions must be met in order to classify a lease as a financing lease:

Any other type of lease is referred to as an operating lease.

Leasing provides several benefits that can be used to attract customers:

One major disadvantage of leasing is the agency cost problem. In a lease, the lessor will transfer all rights to the lessee for a specific period of time, creating a moral hazard issue. Because the lessee who controls the asset is not the owner of the asset, the lessee may not exercise the same amount of care as if it were his/her own asset. This separation between the asset’s ownership (lessor) and control of the asset (lessee) is referred to as the agency cost of leasing. This is an important concept in lease accounting.

Let’s walk through a lease accounting example. On January 1, 2022, Company XYZ signed an eight-year lease agreement for equipment. Annual payments of $28,500 are to be made at the beginning of each year. At the end of the lease, the equipment will revert to the lessor. The equipment has a useful life of eight years and has no residual value. At the time of the lease agreement, the equipment has a fair value of $166,000. An interest rate of 10.5% and straight-line depreciation are used.

Therefore, this is a finance/capital lease because at least one of the finance lease criteria is met during the lease, and the risks/rewards of the asset have been fully transferred. We have determined the proper lease accounting.

| Year | Lease Liability | Interest Expense | Lease Payment | Principal Payment | Balance |

| 0 | $149,317 | $15,678 | $28,500 | $12,822 | $136,495 |

| 1 | $136,495 | $14,332 | $28,500 | $14,168 | $122,327 |

| 2 | $122,327 | $12,844 | $28,500 | $15,656 | $106,671 |

| 3 | $106,671 | $11,201 | $28,500 | $17,299 | $89,372 |

| 4 | $89,372 | $9,384 | $28,500 | $19,116 | $70,256 |

| 5 | $70,256 | $7,377 | $28,500 | $21,123 | $49,133 |

| 6 | $49,133 | $5,159 | $28,500 | $23,341 | $25,792 |

| 7 | $25,792 | $2,708 | $28,500 | $25,792 | $0 |

Year 0 is considered the current year, 2022.

Interest expense is calculated as the opening lease liability balance multiplied by the interest rate of 10.5%, and the lease liability opening balance can be calculated in one of two ways:

The principal payment is the difference between the actual lease payment and the interest expense. The year’s closing balance is calculated as lease liability + interest – lease payment.

January 1, 2022

| DR Equipment | $164,995 |

| CR Cash | $28,500 |

| CR Lease Liability | $136,495 |

The equipment account in the balance sheet is debited by the present value of the minimum lease payments, and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. In some lease agreements, the payment is due at the end of the year, so the lease liability account balance would equal the equipment account balance in this initial entry. The cash entry would not be required at this point, but at the end of the year upon payment.

December 31, 2022

| DR Depreciation Expense | $20,624 |

| CR Accumulated Depreciation | $20,624 |

Straight-line depreciation expense must be recorded for the equipment that is leased. This is based on the calculated equipment cost of $164,995, which is apportioned equally over eight years at $20,624 per year.

DR Interest Expense 15,678

CR Interest Payable 15,678

January 1, 2023

| DR Interest Payable | $14,332 |

| DR Lease Liability | $14,168 |

| CR Cash | $28,500 |

As we debit the lease liability account with the principal payment each year, its balance reduces until it reaches zero at the end of the lease term.

December 31, 2023

| DR Depreciation Expense | $20,624 |

| CR Accumulated Depreciation | $20,624 |

January 1, 2022

| DR Equipment | $164,995 |

| CR Cash | $28,500 |

| CR Lease Liability | $136,495 |

December 31, 2022

| DR Lease Expense | $28,500 |

| CR Lease Liability | $15,678 |

| CR Equipment | $12,822 |

January 1, 2023

| DR Lease Liability | $28,500 |

| CR Cash | $28,500 |

December 31, 2023

| DR Lease Expense | $28,500 |

| CR Lease Liability | $14,332 |

| CR Equipment | $14,168 |

In the operating lease scenario, the lease expense is constant throughout the lease term. The lease liability account is reduced annually by an amount equivalent to the finance lease’s interest expense, and lastly, the equipment account is reduced by the difference between the lease expense and the lease liability change. This last quantity is a plug to get our debits and credits equal, and these amounts will sum up to the lease liability balance over the lease term.

You can read more about lease accounting on the IFRS website .

To keep learning and developing your financial knowledge, we recommend these additional CFI resources:

Get Certified for Financial Modeling (FMVA)®Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.